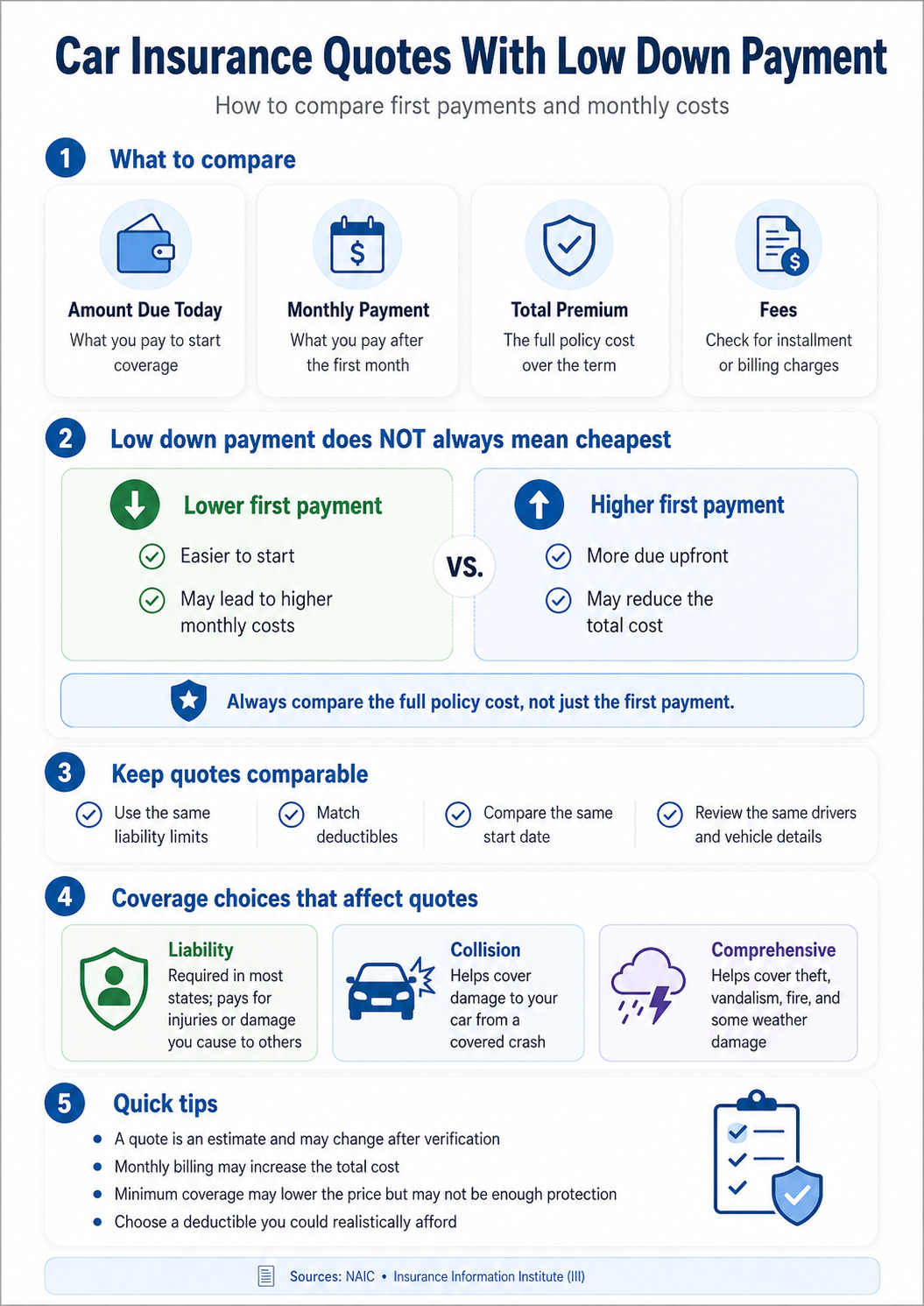

A low first payment does not prove that one car insurance quote is cheaper than another. Compare quotes using the same drivers, vehicles, policy term, limits, deductibles and optional coverages, then calculate the initial completed charge, every later installment and all disclosed charges.

A quote is proposed pricing based on information available at that stage. It is not the same as an accepted application, issued or bound coverage, a temporary insurance card or a declarations page.

“Low down payment” is shopping language rather than a standardized policy type. The insurer, agency or authorized provider determines the actual amount required, payment dates, policy eligibility and effective terms.

Use the same people, vehicles, coverage and policy dates.

Record the initial charge, installments, dates and disclosed charges.

Verify issuance or binding, effective timing and final documents.

What a Car Insurance Quote Does—and Does Not—Prove

A quote shows proposed pricing or terms based on the information entered and verified at that point. It can change when a provider corrects driver, vehicle, address, prior-insurance, discount or coverage information.

| Stage | What it can confirm | What it does not independently confirm |

|---|---|---|

| Preliminary quote | Proposed pricing based on information available so far | Final price, acceptance or active coverage |

| Submitted application | The provider received the application information | That verification or underwriting is complete |

| Payment or authorization | A transaction, hold or scheduled debit may exist | That the insurer issued or bound coverage |

| Binder or temporary ID card | Provider-issued evidence associated with the transaction | That every policy detail is correct |

| Declarations page | Policy period, vehicles, limits, deductibles, premium and other details | That an error should be ignored rather than corrected |

Swipe or scroll horizontally to view all table columns.

The NAIC explains that insurance websites can perform different roles. Some may route information to an agent, while some authorized sites may make coverage available immediately. Others cannot do so even after a premium payment. [1]

Do not drive based only on a quote, application receipt or payment screen. Confirm that coverage has been issued or bound and that the stated effective time has arrived.

Record These Numbers From Every Quote

Policy-term premium

The quoted premium for the complete stated policy period. Record the start and expiration dates.

Initial completed charge

The amount actually collected. Keep it separate from a card hold, authorization or future scheduled debit.

Later installments

Every later payment, including the amount, due date and whether the final installment differs.

Disclosed charges

Any provider-identified billing, installment, agency or other charge applied under the quoted terms.

The NAIC shopping tool recommends asking about payment options and additional charges, comparing at least three quotes and reviewing the declarations page after purchase. [2]

The separate guide to pay monthly car insurance with no deposit explains installment schedules in more detail.

Normalize Every Quote Before Comparing the Price

A lower price is not a fair comparison when the quote uses different people, vehicles, policy dates or coverage. Keep the following inputs as consistent as possible.

| Category | Details to match | Verification question |

|---|---|---|

| Drivers | Named insured, household drivers and proposed exclusions | Are the same people included or excluded in every quote? |

| Vehicles | Year, make, model, VIN, use, mileage and garaging address | Is each quote based on identical vehicle information? |

| Policy timing | Requested effective date, effective time and policy expiration | Do the quotes cover the same stated period? |

| Liability and state-required coverage | The same applicable coverages and limits | Does one quote cost less because its limits are lower? |

| Collision and comprehensive | Both included or excluded, with matching deductibles | Are physical-damage coverages truly equivalent? |

| Optional coverage | The same selected optional protections | Did one quote remove an option to reduce the price? |

| Discounts | Only discounts confirmed in the final quote | Is any discount conditional or awaiting documentation? |

| Billing | Initial charge, installments, due dates and disclosed charges | Is the lower first payment offset by later charges? |

Swipe or scroll horizontally to view all table columns.

The NAIC tool provides worksheets for comparing limits, deductibles, optional coverages and premiums. It advises using the same or similar coverage when collecting quotes. [2]

The page on cheap car insurance with low down payment focuses on deciding whether the complete equivalent quote is actually cheaper.

Illustrative Quote Comparison

The fictional U.S.-dollar amounts below use equivalent coverage for the same six-month policy term. They are educational examples only—not quotes, averages, typical prices or available offers.

| Illustrative quote | Initial completed charge | Later installments | First later due date | Disclosed charges | Scheduled cost | Coverage status |

|---|---|---|---|---|---|---|

| Quote A | USD $75 | 5 × USD $190 | 21 days after start | USD $35 | USD $1,060 | Must still be accepted and issued or bound |

| Quote B | USD $170 | 5 × USD $170 | 30 days after start | USD $0 | USD $1,020 | Must still be accepted and issued or bound |

| Quote C | USD $990 | None | None | USD $0 | USD $990 | Must still be accepted and issued or bound |

Swipe or scroll horizontally to view all table columns.

Quote A requires the least at the beginning but has the highest fictional scheduled cost. Quote C requires the most upfront but has the lowest fictional scheduled cost. The example does not imply that paying in full is always cheaper or that these schedules are offered by any particular provider.

Information to Prepare for Comparable Quotes

Drivers and household

- Names and dates of birth

- Driver’s license information

- Household drivers requested by the provider

- Driving and claims information requested

- Any proposed driver exclusions

Vehicles and use

- Year, make, model and VIN

- Garaging address

- Annual mileage and commute information

- Personal, business or other stated use

- Ownership, loan or lease information

Current or prior insurance

- Current insurer and policy expiration

- Current limits and deductibles

- Any coverage gap information requested

- Prior policy number when requested

- Reason for cancellation or nonrenewal when requested

Requested policy terms

- Requested effective date and time

- Liability and other applicable limits

- Collision and comprehensive deductibles

- Optional coverages to include

- Preferred payment method and frequency

Protect sensitive information. Verify the website, provider identity, licensing resources and privacy terms before submitting a full application or identification documents.

Separate Premium Factors From Billing Factors

A quote can change because of the insurance price, the way that price is divided into payments or both. Treat these as separate categories.

Factors that may affect the premium

- Drivers and driving records

- Vehicle type and use

- Garaging location

- Limits and deductibles

- Optional coverages

- Provider-specific rating factors and discounts

Factors that may affect billing

- Amount allocated to the initial charge

- Number and timing of installments

- Automatic-payment requirements

- Provider-disclosed charges

- Rejected-payment procedures

- Policy changes during the term

The NAIC notes that insurers do not all use the same rating factors and that state rules can limit which factors are permitted. [2]

Request the exact before-and-after premium, initial charge, later installments and out-of-pocket deductible. Do not assume the billing schedule will change in the same proportion as the premium.

Financed or Leased Vehicles Require a Contract Check

A lender or leasing company may require collision, comprehensive or other contractually specified protection. A quote with a lower first payment is not equivalent if it fails to satisfy those requirements.

The CFPB advises consumers financing a vehicle to compare coverage as well as cost. It also explains that a lender may obtain force-placed insurance when required coverage is not maintained; that insurance protects the lender and vehicle rather than the borrower. [3]

Before reducing limits, removing physical-damage coverage or increasing a deductible: review the loan or lease, confirm lienholder details and request the exact quote difference.

Confirm the Provider and Active Coverage

Identify the insurer, agency or quote service

Determine who will issue the policy and whether the website is providing a quote, referral, application or policy transaction.

Verify licensing resources

Use the applicable state insurance department and insurer-search resources rather than relying only on a website or advertisement.

Confirm acceptance and effective timing

Ask whether coverage has been issued or bound and verify the exact effective date and time.

Review the final documents

Check the temporary ID card, binder and declarations page against the drivers, vehicles, coverages, limits, deductibles and billing terms.

The NAIC state directory provides department contact, licensing and complaint resources. [4] Its Consumer Insurance Search provides company information and advises checking the applicable state department for licensing. [5]

Questions about coverage that must begin today are covered in Same-Day Car Insurance With No Down Payment .

Low Down Payment Quote Comparison Checklist

Frequently Asked Questions

Does a low first payment mean the quote is cheaper?

No. Calculate the initial completed charge, all installments and disclosed charges, then compare the result using equivalent coverage and the same policy term.

Is the amount due today always a completed payment?

Not necessarily. It can be an amount to collect, authorize, hold or schedule. Ask what has actually been charged and when any later debit will occur.

Can every installment be different?

A provider’s schedule can use different initial, later or final amounts. Obtain every amount and due date in writing rather than assuming equal monthly payments.

Can the final price change after an online quote?

It can change when the provider verifies or corrects application information, coverage, discounts or other quote inputs. Review the final offer before purchasing.

Does paying the first amount activate coverage?

Not by itself. Confirm that the insurer or authorized provider has issued or bound coverage and verify the effective date and time.

Should I raise a deductible to lower the quote?

Request exact before-and-after figures. A higher deductible may change the premium for applicable coverage, but it also increases the amount you may owe after a covered loss and may be limited by a loan or lease agreement.

How many quotes should I compare?

The NAIC shopping tool recommends obtaining at least three quotes. The comparison is useful only when the quoted drivers, vehicles, coverages, limits and policy terms are aligned.

The Bottom Line

Compare low-down-payment quotes by standardizing the inputs first. Then record the policy-term premium, completed initial charge, later installments, due dates and disclosed charges.

A quote or payment does not independently prove active coverage. Confirm the provider, issuance or binding, effective date and time, and final policy documents before driving.

Explore Available Auto Insurance Quote Pathways

Enter a five-digit U.S. ZIP code. EverQuote will open in another tab, while the SureHit insurance-listings pathway will open in this tab.

CarInsuranceWithNoDownPayment.com is an independent information website, not an insurer, and does not bind, issue or service policies. The site does not guarantee a quote, rate, provider selection, approval, payment schedule, savings or coverage. Not all insurers or options may be represented, and the site may receive compensation from qualifying third-party interactions. Review the Advertiser Disclosure and Privacy Policy.

References

These official resources support the general consumer information in this article. They do not endorse CarInsuranceWithNoDownPayment.com or any commercial service displayed on the site.

- National Association of Insurance Commissioners, Does Your Vehicle Have the Right Protection? Best Practices for Buying Auto Insurance . ↩

- National Association of Insurance Commissioners, A Shopping Tool for Auto Insurance . ↩ ↩ ↩

- Consumer Financial Protection Bureau, What Kind of Auto Insurance Options Are Available When Financing a Car? . ↩

- National Association of Insurance Commissioners, Insurance Departments . ↩

- National Association of Insurance Commissioners, Consumer Insurance Search . ↩

- Federal Trade Commission, .com Disclosures: How to Make Effective Disclosures in Digital Advertising . ↩