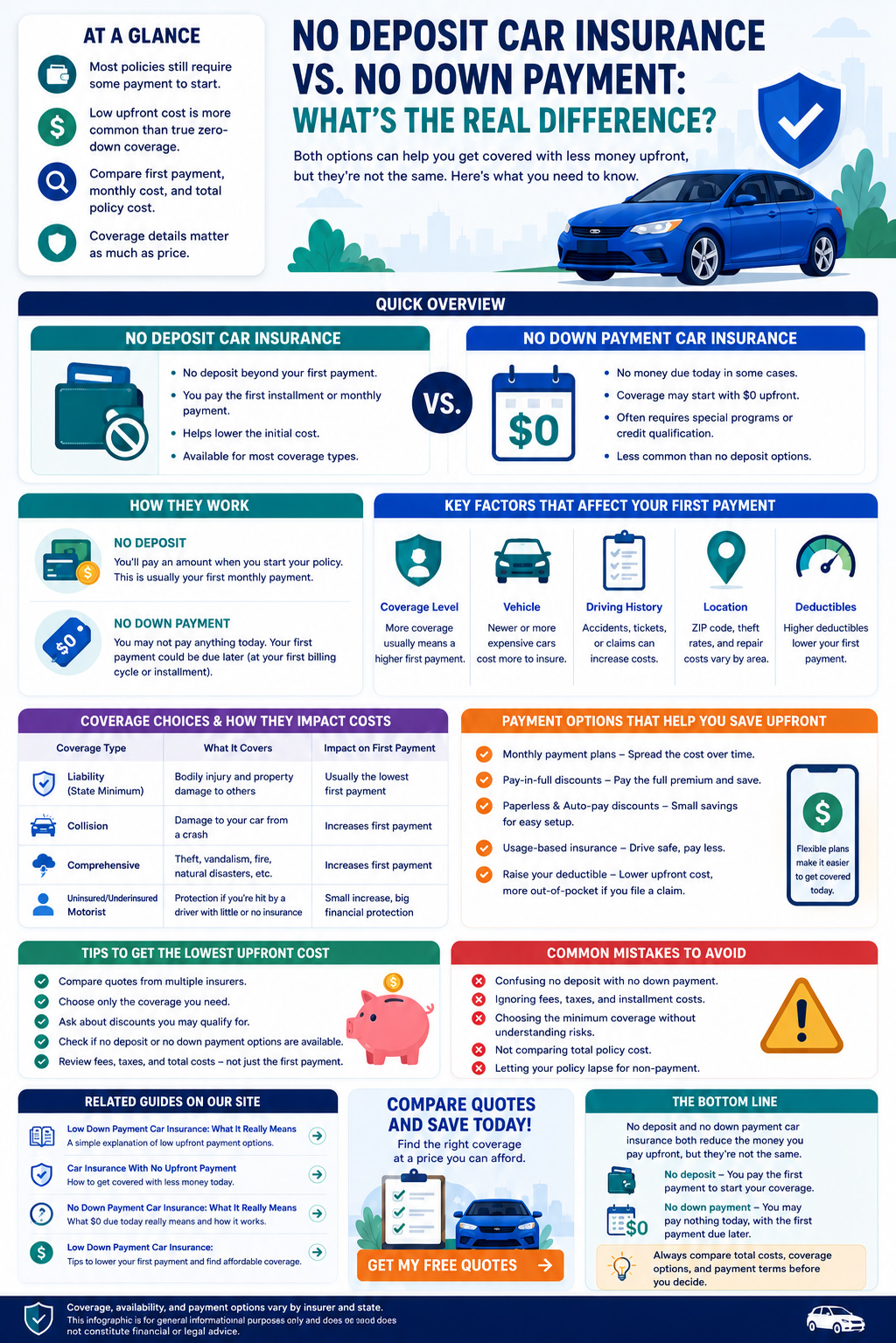

“No down payment car insurance” is a common search and advertising phrase, not a separate standardized type of auto insurance coverage.

It generally describes a policy or payment arrangement with a relatively manageable amount due at the beginning of the policy term. It does not automatically mean that coverage starts for free, that every applicant qualifies or that no payment will be required.

The useful question is not simply whether an offer uses the words “no down payment.” It is how much is due today, what later payments will be, what coverage is included and when the provider confirms that insurance is active.

Confirm the exact initial charge rather than relying on an advertising headline.

Add later installments and disclosed fees to understand the scheduled cost for the policy term.

A submitted form or preliminary quote is not the same as provider-confirmed insurance.

What “No Down Payment” Actually Means

Insurance providers do not necessarily use “down payment” as the formal billing term in their policy documents. Depending on the provider, the amount required at the beginning may be described as an initial premium, first installment, amount due today or another billing charge.

A “no down payment” message may therefore mean that there is no separate deposit in addition to the first scheduled payment. It may also refer to monthly billing that avoids paying the entire six-month or annual premium at once.

It should not be interpreted as a promise that a provider will activate a policy without satisfying its payment, verification and underwriting requirements.

| Term | Common meaning | What to verify |

|---|---|---|

| No down payment | A marketing or search phrase that may describe a lower initial charge or the absence of a separate deposit. | The exact amount due before or when coverage begins. |

| No deposit | There may be no additional deposit beyond the premium or first scheduled installment. | Whether an initial premium, installment or fee is still required. |

| Amount due today | The amount the provider says must be paid at the current stage of the transaction. | What the charge includes and whether payment confirms active coverage. |

| Initial premium | Premium collected at or near the start of the selected policy term. | The policy period, effective date, effective time and later payment schedule. |

| Monthly installments | The premium is divided into scheduled payments rather than paid entirely at once. | The number and amount of payments, due dates and listed fees. |

| Pay in full | The full premium for the selected policy term is paid at the beginning. | Whether a discount applies and which policy term the payment covers. |

Swipe or scroll horizontally to view all table columns.

Drivers specifically looking for ways to reduce the initial amount can review our separate guide to low-down-payment car insurance .

What the Phrase Does Not Guarantee

A headline using “zero down” or similar wording does not establish the final rate, eligibility decision, coverage or payment schedule. Those details depend on the provider, application information, selected coverage and rules applicable to the transaction.

No guaranteed approval

A provider may still verify driver, vehicle, household and prior insurance information before accepting an application.

No promise of free coverage

A low or absent separate deposit does not mean the provider will waive every amount required to start or maintain coverage.

No guarantee of the lowest cost

A smaller amount due today can still be followed by higher installments or additional listed charges.

Watch for incomplete advertising: Be cautious when a page prominently promises “free,” “instant” or “everyone qualifies” without identifying the provider, amount due, payment schedule and conditions.

How to Know Whether Coverage Has Actually Started

An online insurance transaction can pass through several different stages. A visitor should not treat an early stage as proof of an active policy.

The NAIC explains that underwriting is used to evaluate whether an insurer will accept an applicant, while rating is used to determine the price. It also recommends reviewing the declarations page, which identifies information such as the policy period, insured vehicles, coverage limits and deductibles. [1]

- Confirm the insurer or agency name.

- Confirm the named insured.

- Confirm every covered vehicle.

- Confirm covered and excluded drivers.

- Confirm the effective date and time.

- Confirm liability limits and deductibles.

- Confirm the premium and payment schedule.

- Keep the documents supplied by the provider.

Do not cancel an existing policy based only on a quote, form confirmation or payment screen. Confirm that replacement coverage has been issued or bound and verify when it begins.

Compare the Full Payment Schedule, Not Only the First Charge

A lower first payment can improve short-term cash flow, but it does not reveal the total scheduled cost. A useful comparison keeps coverage limits and deductibles as similar as possible and then reviews every scheduled charge.

Illustrative six-payment example

These figures are fictional and do not represent an available quote, insurer or expected rate.

| Illustrative option | Due today | Remaining payments | Listed fees | Scheduled total |

|---|---|---|---|---|

| Option A | $80 | 5 payments of $190 | $20 | $1,050 |

| Option B | $210 | 5 payments of $160 | $0 | $1,010 |

Swipe or scroll horizontally to view all table columns.

Option A requires $130 less at the beginning, but its fictional scheduled total is $40 higher. Coverage would also need to be compared before deciding which option offers better value.

The NAIC shopping tool recommends comparing the same or similar coverages and recording limits, deductibles and premiums for each company. [2]

Our dedicated guide to comparing car insurance quotes with a low initial payment provides a broader quote-comparison checklist.

What Can Affect the Amount Due at the Beginning

The amount shown at the beginning can reflect the overall premium, provider billing structure, selected policy term and amount allocated to the first installment. Underwriting and rating practices differ by insurer and by state.

Where permitted by applicable state law, information considered by an insurer may include:

- Drivers and driving experience.

- Driving and claims history.

- Vehicle type and repair cost.

- Vehicle use and annual mileage.

- Garaging address or rating territory.

- Household drivers.

- Selected limits and deductibles.

- Prior coverage information.

- Available discounts.

- Billing and payment-plan selection.

Not every insurer uses the same factors, and state law may restrict or change how a factor is applied. Accurate application information matters because the proposed rate can change when the provider verifies the drivers, vehicle, location or coverage selections.

Financed and Leased Vehicles May Have Additional Requirements

State minimum liability requirements are not necessarily the only requirements that apply. A lender or leasing company may require collision, comprehensive or other physical-damage protection under the finance or lease agreement.

The CFPB recommends comparing both coverage and cost when financing a vehicle and explains that a lender may obtain force-placed insurance if required coverage is not maintained. [3]

Review the loan or lease agreement before selecting lower coverage limits, removing physical-damage coverage or choosing a deductible. The lender’s requirements are separate from the amount due at the beginning of the insurance policy.

Before Using an Online Quote Form

An insurance information website, marketplace, quote platform, agency and insurer can perform different roles. Check the destination and disclosure before submitting personal information.

Before submitting

Review what information is requested, which company or service will receive it and whether the form includes consent for calls, emails or text messages.

Before purchasing

Verify the provider, review its documents and confirm that the company or licensed professional is authorized in your state.

The NAIC provides a directory for locating state insurance departments, checking insurance professionals and filing complaints. [4]

Review our Privacy Policy before submitting information and our Advertiser Disclosure for information about commercial quote pathways.

Questions to Ask Before Choosing a Policy

These questions keep the focus on the complete policy rather than the advertising phrase.

Frequently Asked Questions

Can car insurance really start with nothing due today?

Do not assume that it can. The amount and timing required to begin coverage depend on the provider and transaction. Confirm the written amount due and the provider’s coverage confirmation before driving.

Does monthly billing mean there is no down payment?

Not necessarily. Monthly billing means the premium is divided into installments. The provider may still require a first installment or another amount at the beginning.

Is a quote proof of insurance?

No. A quote is proposed pricing based on information available at that stage. Proof of coverage should come from documentation supplied by the provider after coverage is issued or bound.

Is the lowest first payment always the cheapest option?

No. Add the remaining installments and listed fees, then compare coverage limits, deductibles and policy conditions. A smaller first charge can still produce a higher scheduled total.

Should I cancel my existing insurance after receiving a quote?

Wait until the replacement provider confirms that coverage has been issued or bound. Verify the effective date and time before ending the existing policy so that you do not unintentionally create a gap.

What should I do if I cannot confirm that the policy is active?

Contact the insurer, agency or licensed producer directly using the contact details supplied with the application or policy documents. Do not rely on the editorial Contact form of this website for urgent policy service.

The Bottom Line

No down payment car insurance is best understood as shopping language for a potentially manageable initial charge—not as a separate coverage type or a guarantee that insurance begins without payment.

Compare the amount due today, later installments, total scheduled cost, coverage limits, deductibles and policy conditions. Most importantly, confirm the effective date and time through documents supplied by the provider.

Explore Available Low-Upfront Quote Pathways

Start with your ZIP code and review the provider, amount due, payment schedule and coverage details before purchasing.

This website is not an insurer and does not guarantee a quote, rate, approval, savings or coverage. The quote pathway may connect you with an independent third-party service, and the website may receive compensation from qualifying interactions.

References

These official resources support the general insurance-shopping information in this article. They do not endorse CarInsuranceWithNoDownPayment.com or any commercial service displayed on the website.

- National Association of Insurance Commissioners, Consumer Auto Insurance Information . ↩

- National Association of Insurance Commissioners, A Shopping Tool for Auto Insurance . ↩

- Consumer Financial Protection Bureau, Auto Insurance Options When Financing a Vehicle . ↩

- National Association of Insurance Commissioners, State Insurance Department Directory . ↩