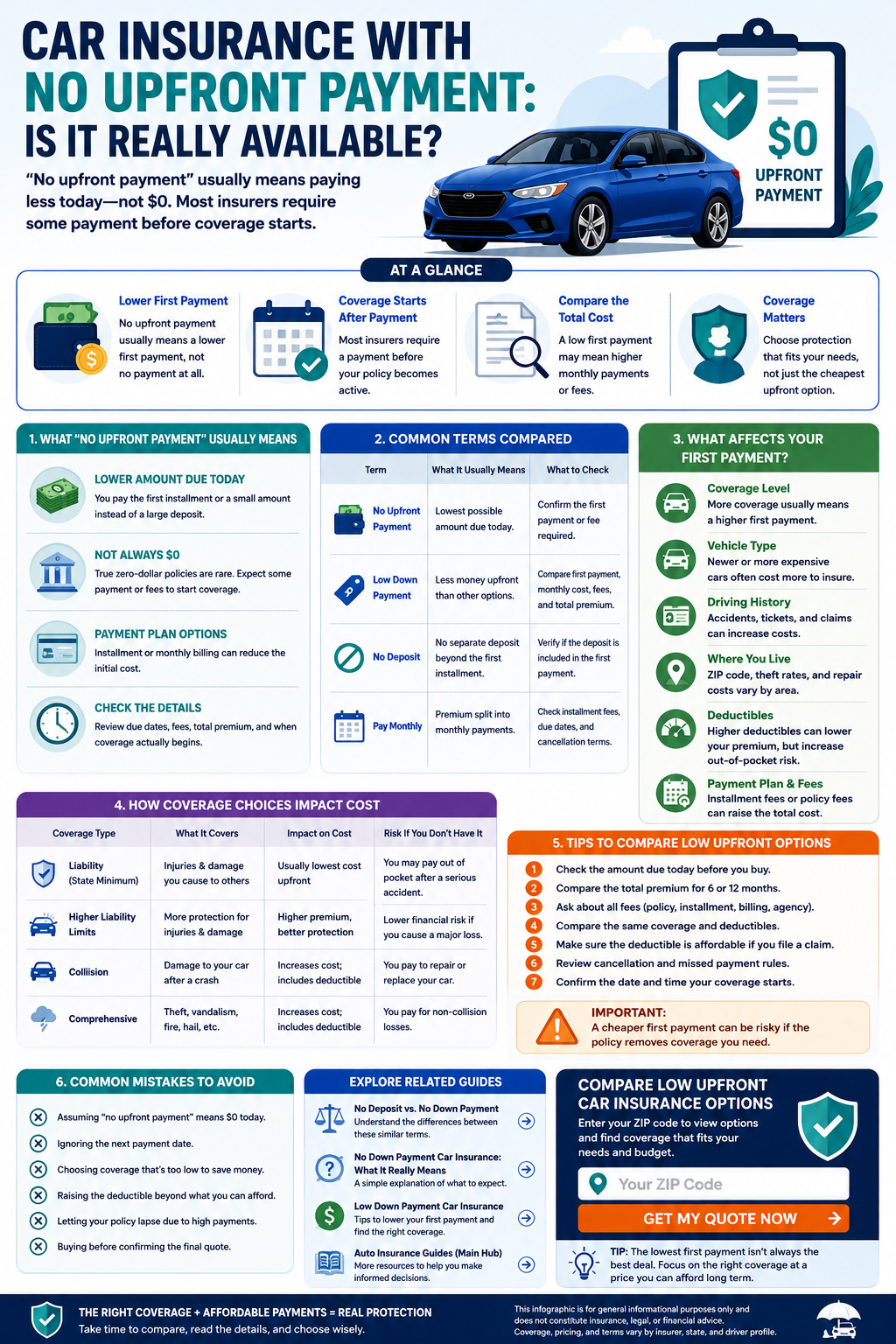

“No deposit car insurance” and “no down payment car insurance” are commonly used shopping phrases, but neither has one uniform meaning across every insurer, agency or quote platform.

The phrases are sometimes used interchangeably. When a provider draws a distinction, “no deposit” may indicate that there is no separate deposit in addition to the initial premium, while “no down payment” may emphasize a relatively low amount due at the beginning.

The wording alone does not tell you the actual cost. Review the amount due today, later installments, fees, coverage, effective date and provider-issued documents before purchasing.

Online publishers and providers may use both phrases for the same monthly-payment arrangement.

Confirm whether an initial premium, installment or separate fee is required.

The payment schedule and provider confirmation are more important than the advertising label.

Are No Deposit and No Down Payment Car Insurance Actually Different?

They can be different, but they are not consistently different. The terms are not standardized coverage names, and the company displaying them should explain exactly what it means.

A provider may use “no deposit” to indicate that it does not require a separate deposit on top of the first premium installment. Another provider may use the same phrase simply to promote monthly billing.

“No down payment” may emphasize a low amount due at the beginning, but it should not be interpreted as a guarantee that no payment is required or that every applicant will qualify.

| Phrase | Possible meaning | What the phrase does not prove | What to verify |

|---|---|---|---|

| No deposit | No separate deposit beyond the initial premium or first installment. | That the transaction has no upfront charge. | Initial premium, separate fees and amount due today. |

| No down payment | A low initial amount or monthly-payment arrangement. | Free coverage, guaranteed approval or zero dollars due. | First charge, later payments and total scheduled cost. |

| Low down payment | A comparatively manageable initial charge. | That the offer has the lowest total premium. | Coverage, installments, fees and policy term. |

| Pay monthly | The premium is divided into installments. | That every installment is equal or fee-free. | Number of payments, due dates and billing conditions. |

| Amount due today | The charge required at the current transaction stage. | That the payment alone confirms active insurance. | What the charge includes and whether coverage was issued. |

Swipe or scroll horizontally to view all table columns.

Practical conclusion: Do not choose between the two phrases. Compare the actual payment schedule and coverage offered under each quote.

For a deeper explanation of the second phrase, read what no down payment car insurance really means .

What to Check Instead of Relying on the Label

The same phrase can describe materially different payment arrangements. Use the provider’s written figures and documents to answer the following questions.

-

How much is due today?

Identify the exact initial charge. -

What does the charge include?

Ask whether it includes premium, installments or separate fees. -

When is the next payment?

A second charge may be scheduled soon after the first. -

How many payments remain?

Confirm the amount and date of every installment. -

What is the policy term?

Determine whether the premium covers six months, twelve months or another period. -

What is the total scheduled cost?

Add the initial charge, remaining installments and disclosed fees. -

Which coverage is included?

Compare limits, deductibles and exclusions. -

When does insurance begin?

Verify the effective date and time in provider documentation.

The NAIC recommends comparing coverages as well as costs, asking about payment options and any extra charge for monthly or quarterly billing, and obtaining multiple quotes using comparable information. [1]

Drivers focused primarily on lowering the initial charge can review the separate guide to low-down-payment car insurance .

A Payment or Quote Does Not Automatically Confirm Active Coverage

An online interaction may represent only one stage of an insurance transaction. Confirm what stage you have reached before driving or canceling another policy.

The NAIC distinguishes underwriting—the process of evaluating an applicant’s risk—from rating, which assigns the price. It also explains that auto insurance is a legal agreement covering specified risks while the policy is active and within its limits. [2]

Do not cancel existing insurance based only on an estimate, quote, form confirmation or payment screen. Confirm that the replacement provider has issued or bound coverage and verify its effective date and time.

Compare the Total Scheduled Cost

A lower amount due today can improve short-term cash flow without being the least expensive option over the complete policy term.

Illustrative six-payment comparison

The following amounts are fictional examples in U.S. dollars. They do not represent an available quote or expected insurance price.

| Illustrative option | Due today | Remaining payments | Listed fees | Scheduled total |

|---|---|---|---|---|

| Option A | $75 | 5 payments of $195 | $25 | $1,075 |

| Option B | $210 | 5 payments of $165 | $0 | $1,035 |

Swipe or scroll horizontally to view all table columns.

Option A requires $135 less initially but has a fictional scheduled total that is $40 higher. Coverage would still need to be compared before choosing between the options.

For a more detailed quote checklist, visit the guide to comparing car insurance quotes with low initial payments .

Why the First Payment Can Differ

The first charge is connected to the overall premium, billing plan, provider requirements and selected policy term. It can therefore differ between applicants and providers.

Underwriting and rating practices vary by insurer and state. Where permitted by applicable state law, information considered may include:

- Drivers and driving experience.

- Driving and claims history.

- Vehicle type and repair cost.

- Vehicle use and annual mileage.

- Garaging address or rating territory.

- Household drivers.

- Selected limits and deductibles.

- Prior coverage information.

- Available discounts.

- Billing-plan selection.

The NAIC states that not every insurer uses the same factors and that the factors used to determine premiums differ by state. [1]

Incomplete or inaccurate information can also change the proposed price after the provider verifies drivers, vehicles, location and coverage selections.

Coverage Still Matters More Than the Advertising Phrase

A quote with a small initial charge may use different limits, deductibles or optional coverages from another quote. Compare equivalent protection before deciding that one offer is less expensive.

Liability limits

Minimum requirements vary by state. Lower limits can leave more accident-related costs outside the policy.

Physical-damage coverage

Collision and comprehensive may have separate deductibles and can be required by a lender or lease agreement.

Optional protection

Rental reimbursement, roadside assistance and other options can change both coverage and price.

The CFPB recommends comparing coverage as well as cost when financing a vehicle. It also explains that a lender may obtain force-placed insurance if required vehicle coverage is not maintained. [3]

Before Using an Online Quote Form

An insurer, agency, licensed producer, quote platform, marketplace and independent information website can perform different roles. Check the destination and its disclosure before entering personal information.

Before submitting

Review which service receives the information, what data will be transmitted and whether the form includes consent for calls, emails or text messages.

Before purchasing

Confirm the company or licensed professional, examine provider-issued documents and verify licensing through the applicable state insurance authority.

The NAIC directory can be used to locate state insurance departments, search for insurance professionals or file a complaint. [4]

Review the Privacy Policy before submitting information and the Advertiser Disclosure for information about commercial relationships.

Frequently Asked Questions

Are no deposit and no down payment car insurance the same?

They may be used for the same payment arrangement. When a provider distinguishes them, no deposit may mean no separate deposit beyond the initial premium, while no down payment may emphasize a low initial charge. Always review the written payment schedule.

Does no deposit mean zero dollars due today?

Not necessarily. An initial premium, first installment or other disclosed charge may still be required. Confirm the exact amount due before assuming that the transaction has no upfront cost.

Is a quote confirmation proof of insurance?

No. A quote or form confirmation may only show that information was submitted or that pricing was proposed. Confirm issued or bound coverage through documentation from the provider.

Why can the first payment differ from an advertised amount?

Advertising may show an example, starting amount or simplified description. The actual charge can depend on verified application information, selected coverage, billing structure and disclosed fees.

Is monthly billing always more expensive?

Not always. Some providers charge installment or billing fees, while others may offer different discounts or arrangements. Compare the complete payment schedule rather than assuming one method always costs more.

How should I confirm when coverage begins?

Review the binder, declarations page, insurance card or other documentation supplied by the provider and verify the effective date and time directly with the insurer or licensed professional.

The Bottom Line

No deposit and no down payment car insurance are flexible shopping phrases, not dependable descriptions of two separate policy types. They may refer to the same arrangement or be defined differently by the company displaying them.

Compare the exact initial charge, payment schedule, total cost, limits, deductibles, fees and effective terms. The provider’s written documents are more important than the wording used in an advertisement.

Explore Available Low-Upfront Quote Options

Enter a five-digit ZIP code to open two independent third-party quote options. EverQuote will open first, followed by SureHit as the primary visible quote destination.

Enter a valid five-digit U.S. ZIP code.

CarInsuranceWithNoDownPayment.com is not an insurer and does not guarantee a quote, rate, approval, savings or coverage. The website may receive compensation from qualifying third-party interactions. Review the Advertiser Disclosure and Privacy Policy .

References

These official resources support the general insurance and consumer information presented in this article. They do not endorse CarInsuranceWithNoDownPayment.com or its commercial partners.

- National Association of Insurance Commissioners, A Shopping Tool for Auto Insurance . ↩

- National Association of Insurance Commissioners, Auto Insurance . ↩

- Consumer Financial Protection Bureau, Auto Insurance Options When Financing a Vehicle . ↩

- National Association of Insurance Commissioners, State Insurance Department Directory . ↩