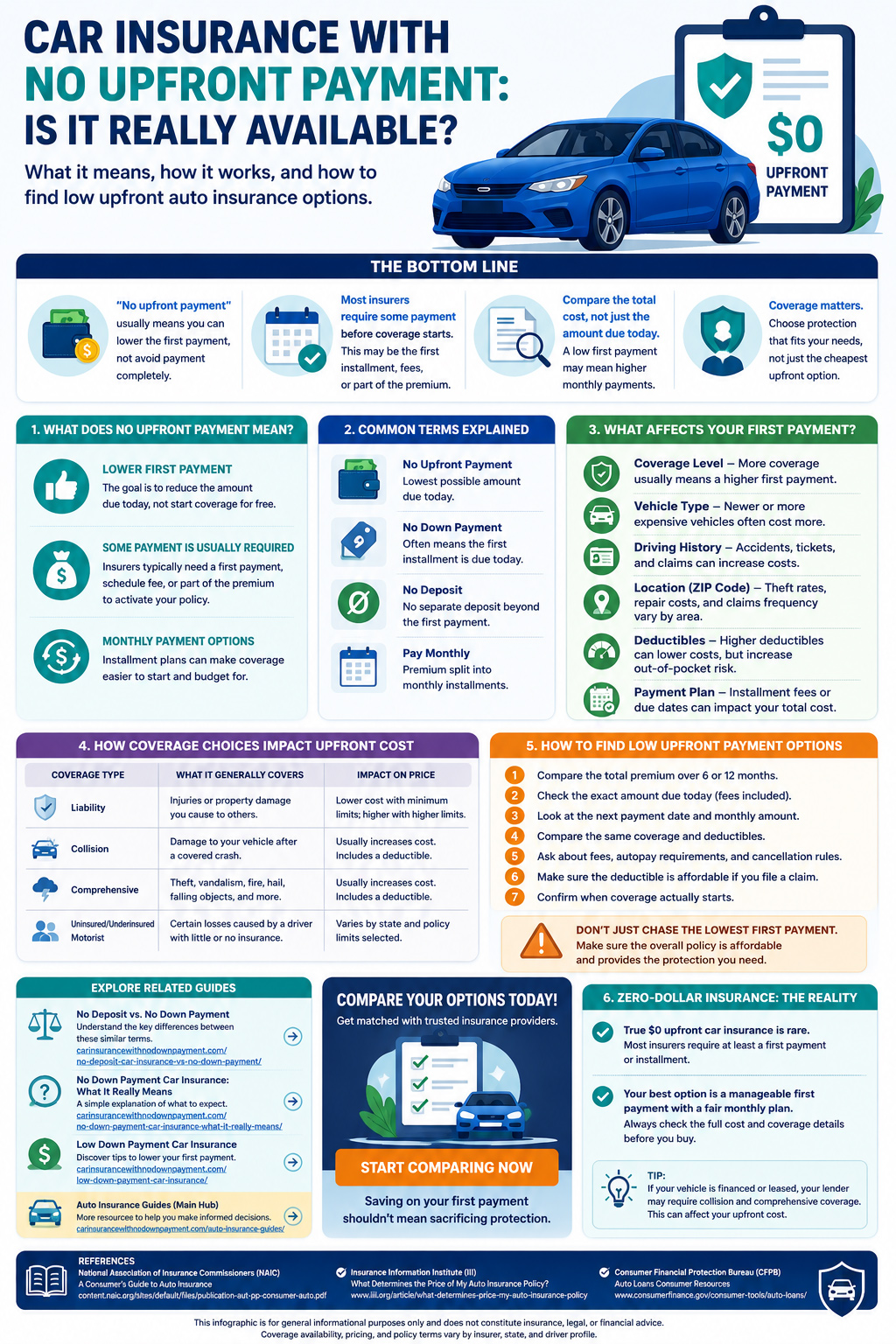

Low down payment car insurance is shopping language for a policy or billing arrangement with a comparatively manageable amount due at the beginning. It is not a standardized coverage type, and it does not guarantee that insurance starts with no payment.

Lowering the first payment and lowering the total premium are different goals. A provider may reduce the amount due today by spreading more of the premium across later installments, while another option may require more initially but cost less over the complete policy term.

The useful comparison is therefore the exact initial charge, what it includes, the remaining payment schedule, disclosed fees, equivalent coverage and the provider-confirmed effective date and time.

Confirm the exact amount due and whether it includes premium or separate charges.

Add later installments and disclosed fees for the full quoted policy term.

Compare the same limits, deductibles, drivers, vehicles and effective date.

What Low Down Payment Car Insurance Means

The phrase generally describes an offer with a lower initial charge than another available payment arrangement. The provider may instead use terms such as initial premium, first installment or amount due today.

The label does not establish a universal dollar amount or percentage. It also does not prove that the offer has the lowest premium, that every applicant qualifies or that payment alone confirms active insurance.

Keep the terms separate: the premium is the price charged for insurance during the policy term; the billing plan determines when portions of that premium and any disclosed charges are due.

For a definition-focused explanation, review what no down payment car insurance really means . The terminology comparison belongs in the separate guide to no deposit versus no down payment car insurance .

Seven Ways to Look for a Lower First Payment

No method guarantees a particular amount. These steps help identify whether a lower initial charge is genuine, sustainable and attached to suitable coverage.

Obtain at least three comparable quotes

Use the same drivers, vehicles, garaging address, policy term, effective date, limits, deductibles and optional coverages. The NAIC recommends contacting more than one insurer or agent and obtaining at least three quotes. [1]

Request the complete payment breakdown

Ask for the amount due today, the next due date, the number and amount of remaining payments and every disclosed billing or installment charge.

Compare monthly and pay-in-full arrangements

A monthly option may reduce the initial charge, while paying more at the beginning may reduce later obligations or qualify for a provider-specific discount. Verify the actual figures instead of assuming either method is cheaper.

Verify discounts in the final quote

Ask which discounts are available and which have already been applied. Safe-driving, multi-policy, multi-vehicle, electronic-document or payment discounts are provider-specific and may be subject to verification.

Review coverage without removing required protection

Compare the cost of optional coverages separately, but retain coverage required by state law and any loan or lease agreement. Do not compare a liability-only quote with a quote containing collision and comprehensive and call the difference a billing saving.

Test deductible options with exact quote figures

A higher collision or comprehensive deductible can reduce the premium, but the change may or may not materially reduce the initial installment. Compare the provider’s exact before-and-after figures and choose only a deductible you could reasonably pay after a covered claim.

Keep application information complete and consistent

Use accurate driver, vehicle, household, mileage, address and prior-insurance information. A preliminary amount can change when the provider verifies the application.

Illustrative Comparison of Three Payment Schedules

The fictional examples below use equivalent coverage and a six-payment term. They are educational examples only and are not quotes, available offers or expected prices.

| Illustrative option | Due today | Remaining payments | Listed fees | Scheduled total | Initial share |

|---|---|---|---|---|---|

| Option A | $75 | 5 × $195 | $25 | $1,075 | 7.0% |

| Option B | $190 | 5 × $165 | $0 | $1,015 | 18.7% |

| Option C | $140 | 5 × $175 | $10 | $1,025 | 13.7% |

Swipe or scroll horizontally to view all table columns.

Option A has the smallest fictional initial payment but the highest scheduled total. Option B requires more initially but has the lowest scheduled total. Option C falls between them. The preferred arrangement depends on both affordability and equivalent coverage—not on the first charge alone.

A broader comparison worksheet is available in the guide to comparing car insurance quotes with low initial payments .

Coverage and Lender Requirements Come First

State minimum requirements vary, and a lender or leasing company may require physical-damage coverage under the finance or lease agreement. Reducing or removing coverage solely to obtain a smaller initial charge can therefore create legal, contractual or financial exposure.

Liability coverage

Compare bodily-injury and property-damage limits separately and confirm the requirements that apply in your state.

Collision and comprehensive

These coverages commonly have separate deductibles and may be required by a lender or lease agreement.

Optional coverage

Review the separate cost and value of options such as rental reimbursement or roadside assistance instead of removing them automatically.

The NAIC advises comparing the same or similar coverage and notes that state law and auto lenders can require particular coverages. [1] The CFPB explains that a lender may obtain force-placed insurance when required coverage is not maintained; that coverage can be more expensive and may protect primarily the lender’s interest. [2]

Before changing collision, comprehensive or a deductible: review the loan or lease agreement and ask the provider to show the exact change in premium, initial payment and remaining installments.

Confirm Active Coverage Before Cancelling Another Policy

An estimate, quote, submitted application or payment screen does not necessarily prove that coverage has been issued or bound. Confirm the provider, named insured, listed drivers, covered vehicles, effective date, effective time, limits, deductibles and payment schedule.

The NAIC recommends reading the declarations page after receiving the policy. That page commonly identifies the policy period, coverages, limits, deductibles, discounts and total premium. [1]

- Confirm the insurer or licensed provider.

- Confirm the named insured and all listed drivers.

- Confirm every covered vehicle.

- Review any driver exclusions.

- Verify the effective date and time.

- Review limits and deductibles.

- Save the binder, declarations page and insurance card.

- Cancel prior insurance only after replacement coverage is confirmed.

State insurance departments can answer general regulatory questions and provide licensing or complaint information. [3]

Checklist Before Choosing a Low-Initial-Payment Option

General answers about payments, coverage and quote terminology are also available in the auto insurance FAQ.

Frequently Asked Questions

Can an insurer offer a lower initial payment?

A provider may offer a payment arrangement with a comparatively smaller amount due at the beginning. Availability, eligibility and the amount depend on the provider, state, application, coverage and billing plan.

Does a lower first payment mean a lower premium?

No. The provider may simply allocate more of the premium to later installments. Compare the premium for the complete policy term and the scheduled total, including disclosed charges.

Can a higher deductible reduce the first payment?

A higher collision or comprehensive deductible may reduce the premium, but the effect on the initial installment depends on the provider’s billing structure. Request exact before-and-after figures and choose only a deductible you could reasonably pay after a covered claim.

What should I ask about the second payment?

Ask for its due date, amount, payment method and whether it includes an installment charge. Do not assume it will arrive exactly one month after the initial payment.

Does submitting a payment confirm active insurance?

Not by itself. Confirm issued or bound coverage and verify the effective date and time in documentation supplied by the insurer, agency or licensed producer.

Should I cancel my old policy after receiving a quote?

Wait until replacement coverage has been issued or bound and its effective date and time are confirmed. This helps avoid an unintended gap.

The Bottom Line

A lower initial payment can make the beginning of a policy more manageable, but it is only one part of the transaction. Compare at least three equivalent quotes, separate premium factors from billing factors and calculate the scheduled cost for the entire quoted policy term.

Keep state and lender requirements intact, verify discounts and fees, choose a realistic deductible and confirm coverage in provider-issued documents before cancelling another policy.

Explore Available Low-Upfront Quote Options

Enter a five-digit U.S. ZIP code. EverQuote will open in a new tab, and the SureHit listings pathway will become the visible page in this tab.

This action sends your ZIP code and referral identifiers to two independent third-party services.

CarInsuranceWithNoDownPayment.com is not an insurer and does not guarantee a quote, rate, approval, savings, payment amount or coverage. The site may receive compensation from qualifying third-party interactions. Review the Advertiser Disclosure and Privacy Policy.

References

These official resources support the general consumer information in this article. They do not endorse CarInsuranceWithNoDownPayment.com or any commercial service displayed on the site.

- National Association of Insurance Commissioners, A Shopping Tool for Auto Insurance. ↩ ↩ ↩ ↩

- Consumer Financial Protection Bureau, Auto Insurance Options When Financing a Vehicle. ↩

- National Association of Insurance Commissioners, State Insurance Department Directory. ↩