A transaction showing $0 due immediately may be possible under specific provider terms, but “car insurance with no upfront payment” is not a standardized auto insurance product and should not be treated as a universal promise.

A $0 screen can mean several different things: you may still be at the quote stage, a payment may be scheduled for a future date, a card may be authorized without an immediate charge, or the provider may be using promotional language for a low—not zero—initial payment.

The sources reviewed do not establish a nationwide frequency for true $0-due-at-start auto insurance arrangements. The safe conclusion is that availability and eligibility must be confirmed for the specific applicant, provider, state, payment plan and effective date.

A conditional offer may exist without being available to every applicant.

A quote or payment screen does not by itself confirm active coverage.

Verify the first debit, full schedule, effective time and provider documents.

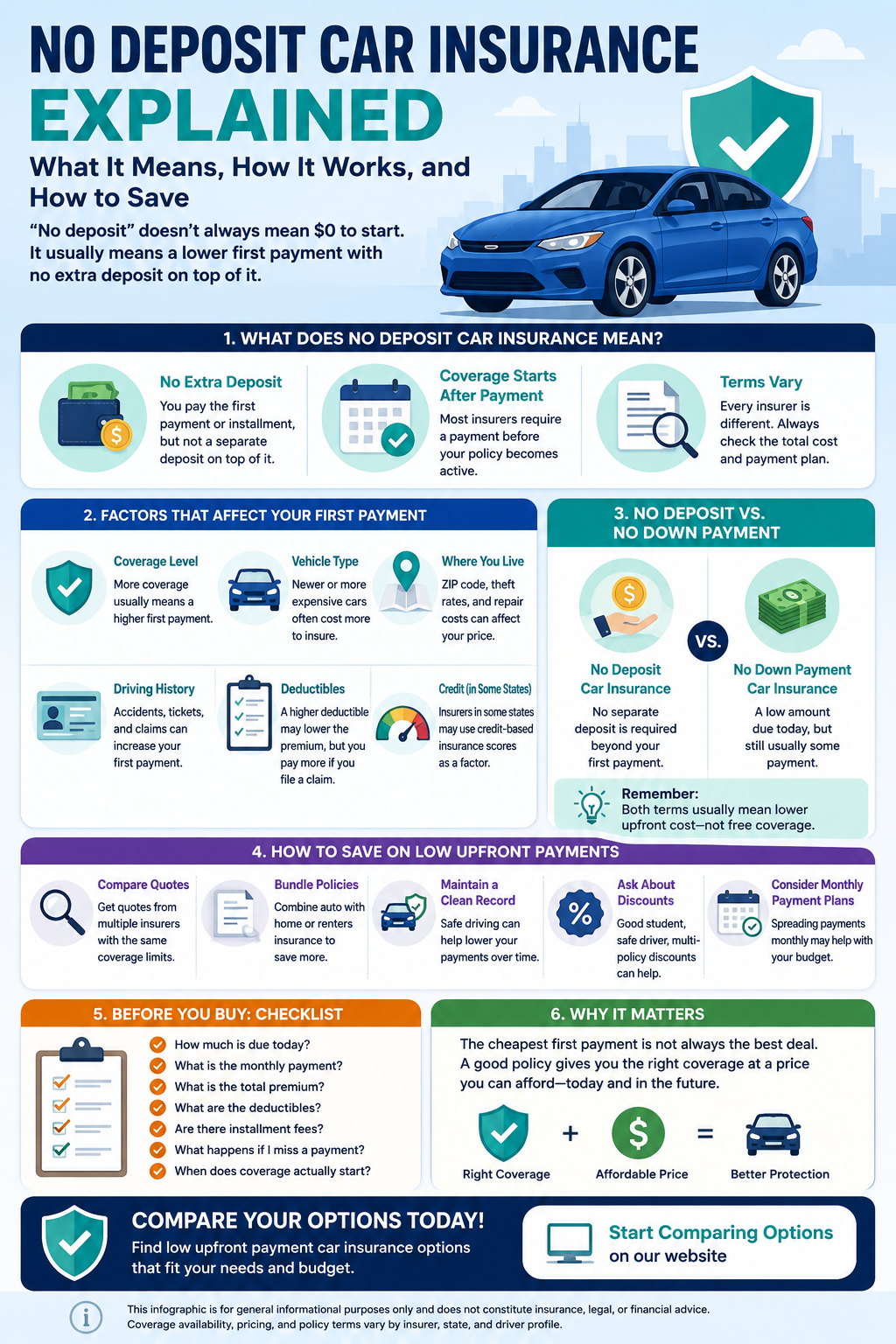

Is Car Insurance With No Upfront Payment Really Available?

It may be available in a particular transaction, but the phrase alone does not prove that an insurer will issue coverage without collecting or scheduling a payment. It also does not prove that every applicant qualifies.

Regulators do not define “no upfront payment” as a standard coverage category. Auto insurance documents are more likely to identify a premium, policy period, amount due, installment schedule and effective date.

The NAIC notes that online insurance websites do not all perform the same role. Some websites send information to an agent, not all provide an immediate quote, and some cannot make coverage available immediately even after a premium payment has been made. [1]

Treat any $0-upfront message as conditional until the provider confirms in writing what will be charged, when it will be charged and whether coverage has been issued or bound.

For a broader explanation of “no down payment” language, read what no down payment car insurance really means .

What a $0-Due-Today Message May Actually Mean

The following are possible transaction scenarios to clarify with the provider. They are not universal definitions and do not establish that a policy is active.

| Possible scenario | What may be happening | What to ask | Does it prove coverage? |

|---|---|---|---|

| Quote stage only | No payment is requested because no policy has been issued. | Is this an estimate, quote or accepted application? | No. |

| Future debit date | The first installment may be scheduled after the current date. | What amount will be debited, and on what date? | Not by itself. |

| Payment authorization | A card or bank account may be authorized for a later charge. | Is this an authorization, hold or completed payment? | Not by itself. |

| Credit or adjustment | A provider-specific credit may reduce the amount currently collected. | Is the credit conditional, temporary or recoverable later? | Not by itself. |

| Low payment described loosely | The headline may refer to a comparatively small initial charge rather than $0. | What is the exact amount due before the effective date? | No. |

Swipe or scroll horizontally to view all table columns.

Do not rely on the headline alone. “No upfront payment,” “zero down,” “no deposit” and similar phrases can be used differently by different websites and providers.

The terminology itself is compared separately in No Deposit Car Insurance vs. No Down Payment Car Insurance .

Seven Details to Verify Before Treating the Offer as Real

The current transaction stage

Confirm whether you are viewing an estimate, quote, application, binder or issued policy.

The exact amount due now

Ask whether the displayed amount includes premium, an installment, a fee, a credit or only a payment authorization.

The first actual debit

Obtain the amount, date and payment method for the first completed charge—not only the amount shown on the current screen.

The full payment schedule

Review the number, amount and due date of later installments, including any disclosed billing or installment charges.

The effective date and time

Confirm exactly when coverage begins. A payment authorization or submitted application is not the same as provider-confirmed coverage.

The insurer and policy details

Verify the insurer, named insured, drivers, vehicles, limits, deductibles, exclusions and policy period.

The proof supplied by the provider

Save the binder, declarations page, insurance card and payment schedule. Contact the insurer, agency or licensed producer if the documents are incomplete or inconsistent.

The NAIC shopping tool recommends asking about payment options and extra charges, comparing the same or similar coverage and reviewing the declarations page, including the policy period, limits, deductibles and premium. [2]

Continuity reminder: do not cancel existing insurance based only on an estimate, quote, application receipt or payment screen. First confirm that replacement coverage has been issued or bound and verify its effective date and time.

$0 Today Can Still Lead to a Higher Scheduled Cost

Delaying the first debit does not eliminate the premium. The remaining payments may be larger, arrive sooner than expected or include disclosed installment charges.

Compare the complete quoted policy term—not only the current screen. The guide to comparing car insurance quotes with low initial payments provides a more detailed quote worksheet.

Coverage and Financing Requirements Still Apply

A no-upfront-payment message does not change state insurance requirements or the terms of an auto loan or lease. Quotes should be compared using equivalent limits, deductibles and optional coverages.

State requirements

Minimum required coverages vary by state and should be verified with the applicable regulator or motor-vehicle authority.

Loan or lease requirements

A lender or leasing company may require collision, comprehensive or other contractually specified protection.

Equivalent comparisons

A quote with less coverage is not a fair price comparison merely because its initial charge is smaller.

The CFPB advises consumers financing a vehicle to compare coverage as well as cost. It also explains that a lender can acquire force-placed insurance if required coverage is not maintained, and that this protection is for the lender and vehicle rather than the borrower. [3]

Strategies for reducing a first payment without confusing it with a reduction in total premium are covered in Low Down Payment Car Insurance: How to Lower Your First Payment .

Check the Role of an Online Quote Website

An insurer, agency, licensed producer, marketplace, referral website and insurance-listings service can perform different roles. Before entering information, identify the destination and read the disclosure near the relevant button or form.

- Which company or service receives the ZIP code?

- Will the visitor leave the current website?

- Will more than one external destination open?

- Does the site receive compensation?

- Does submitting information authorize calls, emails or texts?

- Does the external service provide a quote, listing or referral?

The FTC states that disclosures needed to prevent an online claim from being misleading should be clear and conspicuous across the devices and platforms used to view the advertisement. [4]

State insurance departments can provide regulator contact details, licensing searches and complaint information. [5]

Frequently Asked Questions

Can a provider show $0 due today?

It may happen in a specific transaction, but the screen must be interpreted carefully. Confirm whether you are still at the quote stage, whether a payment is scheduled later and whether coverage has actually been issued or bound.

Does $0 due today mean the policy is free to start?

Not necessarily. Premium may be collected later, divided among installments or reduced temporarily by a provider-specific credit. Ask for the complete schedule and all disclosed charges.

Can a provider authorize my card without charging it immediately?

A provider may use an authorization or future payment instruction, but the specific process depends on that provider. Ask whether the transaction is an authorization, hold, scheduled debit or completed payment.

Does paying something prove that coverage is active?

No. Payment alone may not confirm that the application has been accepted. Verify issued or bound coverage and the effective date and time in documents supplied by the provider.

Should I cancel my existing policy after receiving a $0-upfront quote?

Wait until replacement coverage has been issued or bound and its effective date and time have been confirmed. A quote or application receipt is not enough.

Can financed or leased vehicles qualify?

Eligibility and billing depend on the provider, while the required coverage depends on state law and the loan or lease agreement. A low or deferred first payment does not remove contractual coverage requirements.

The Bottom Line

Car insurance with no upfront payment may be possible under a specific provider arrangement, but it is not a standardized product and cannot be promised universally. A $0 message may describe a quote stage, future debit, payment authorization, credit or loosely worded low initial payment.

Before relying on the offer, verify the completed charge, first debit date, full schedule, coverage details and effective date and time in provider-issued documents.

Explore Available Auto Insurance Quote Pathways

Enter a five-digit U.S. ZIP code. EverQuote will open in another tab, while the SureHit insurance-listings pathway will become the visible page in this tab.

This action sends your ZIP code and referral identifiers to two independent third-party services.

CarInsuranceWithNoDownPayment.com is not an insurer and does not guarantee a quote, rate, approval, savings, payment amount or coverage. The site may receive compensation from qualifying third-party interactions. Review the Advertiser Disclosure and Privacy Policy .

References

These official resources support the general consumer information in this article. They do not endorse CarInsuranceWithNoDownPayment.com or any commercial service displayed on the site.

- National Association of Insurance Commissioners, Does Your Vehicle Have the Right Protection? Best Practices for Buying Auto Insurance . ↩

- National Association of Insurance Commissioners, A Shopping Tool for Auto Insurance . ↩

- Consumer Financial Protection Bureau, Auto Insurance Options When Financing a Vehicle . ↩

- Federal Trade Commission, .com Disclosures: How to Make Effective Disclosures in Digital Advertising . ↩

- National Association of Insurance Commissioners, State Insurance Department Directory . ↩